Brand-name drugs can cost hundreds-even thousands-of dollars a month. If you’re insured but still struggling to afford your medication, you’re not alone. Many people don’t know that the drug manufacturer itself may offer financial help through manufacturer savings programs. These aren’t charity programs. They’re designed to help you pay less out of pocket right now, but they also help companies keep you on their brand instead of switching to cheaper generics. Used correctly, these programs can cut your monthly bill by 70% to 85%. Used wrong, they can leave you shocked when your discount suddenly disappears.

What Are Manufacturer Savings Programs?

Manufacturer savings programs are tools created by pharmaceutical companies to reduce your out-of-pocket cost for brand-name drugs. There are two main types: copay cards (or coupons) and patient assistance programs (PAPs). Copay cards are the most common. You sign up online, get a digital or physical card, and present it at the pharmacy. The program pays part of your cost, so you pay much less-sometimes as little as $10 or $25 per prescription.

Patient assistance programs are usually for people with lower incomes. They may give you free medication for up to a year. But most people use copay cards because they’re easier to access and work with private insurance.

These programs are everywhere. According to 2023 industry data, 98% of major brand-name drugs offer some kind of savings help. Drugs for diabetes, asthma, rheumatoid arthritis, and high cholesterol almost always have them. But here’s the catch: you can’t use them if you’re on Medicare, Medicaid, or any other federal health program. The law bans it. That’s why these programs only work if you have private insurance through your job or bought on the marketplace.

How Do They Actually Work?

It sounds simple: you get a coupon, go to the pharmacy, and pay less. But behind the scenes, there’s a whole system.

When you sign up for a copay card, you enter your insurance info and prescription details. The manufacturer’s system checks if your plan allows it. Then, when the pharmacy processes your claim, a third-party administrator-like ConnectiveRx or Prime Therapeutics-steps in. They verify you’re eligible, apply the discount, and the manufacturer pays them back.

You don’t pay anything extra. The pharmacy doesn’t charge you the full price. You just pay the reduced amount. The rest is covered by the drug maker.

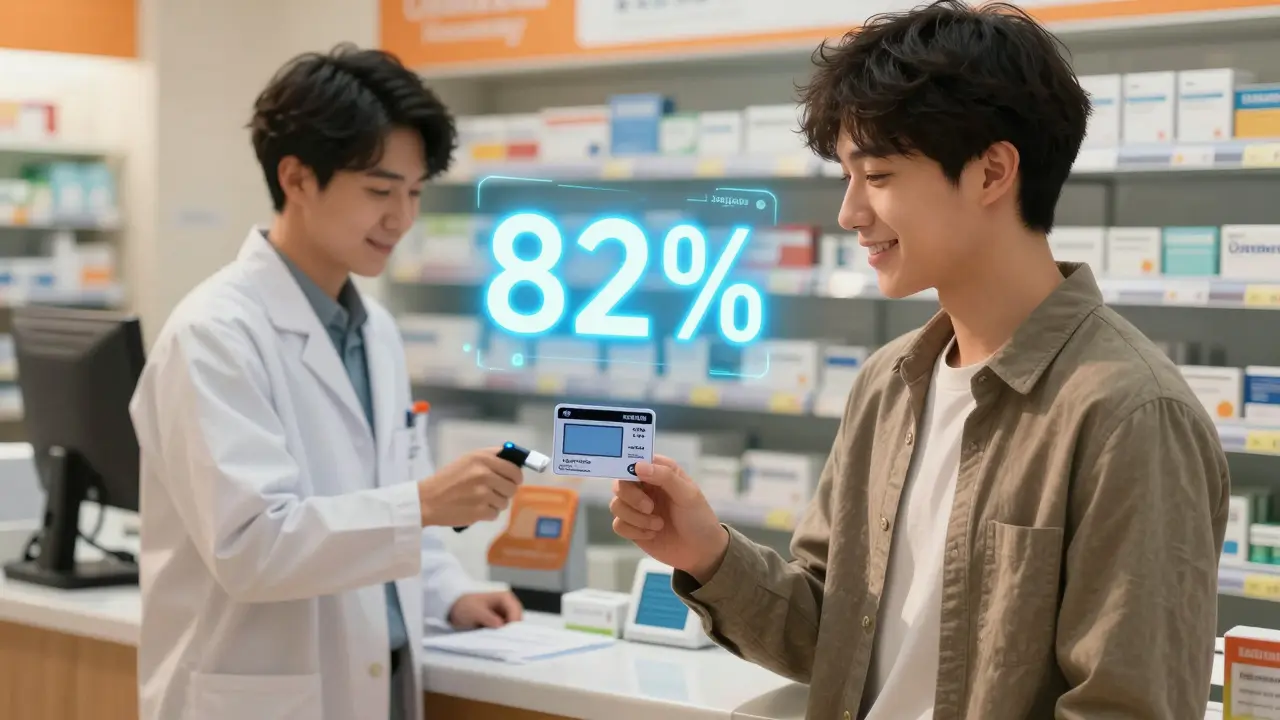

For example, a diabetes drug like Jardiance might cost $562.50 per month without help. With the manufacturer’s copay card, you pay $100. That’s a 82% drop in your out-of-pocket cost. That’s the power of these programs.

Who Can Use Them?

You can use these programs if:

- You have private health insurance (not Medicare, Medicaid, or VA)

- You’re prescribed a brand-name drug that offers a savings program

- Your insurance plan doesn’t block manufacturer discounts (more on that below)

You cannot use them if:

- You’re on Medicare Part D or Medicaid

- You have no insurance

- Your drug doesn’t have a program (rare, but some older drugs don’t)

Some plans, especially those from large employers, have something called an accumulator adjustment program. This means the manufacturer discount doesn’t count toward your deductible or out-of-pocket maximum. So even though you pay less now, you still have to meet your full deductible later. That can cost you thousands more by year’s end. About 87% of large employers used these programs in 2022.

How to Find and Enroll

Step 1: Find the right program.

Go to the drug manufacturer’s official website. Search for your drug name + “savings” or “patient assistance.” For example, search “Humira savings program” or “Ozempic copay card.” Most companies have a dedicated page. You can also use trusted aggregators like GoodRx, but always double-check the manufacturer’s site for the most accurate info.

Step 2: Check eligibility.

The form will ask for your insurance details, name, date of birth, and prescription info. It’s quick-usually under 5 minutes. The system will tell you right away if you qualify. If you’re denied, it usually says why: “Medicare not eligible” or “Insurance not participating.”

Step 3: Get your card.

If approved, you’ll get a digital card via email or text. Some programs mail a physical card. Save it. Take a screenshot. Add it to your phone’s wallet. You’ll need it every time you refill.

Step 4: Use it at the pharmacy.

When you pick up your prescription, hand the pharmacist your card or show the digital version. They’ll process it. You pay the reduced price. No extra steps.

What You Need to Watch Out For

These programs aren’t perfect. Here are the biggest traps:

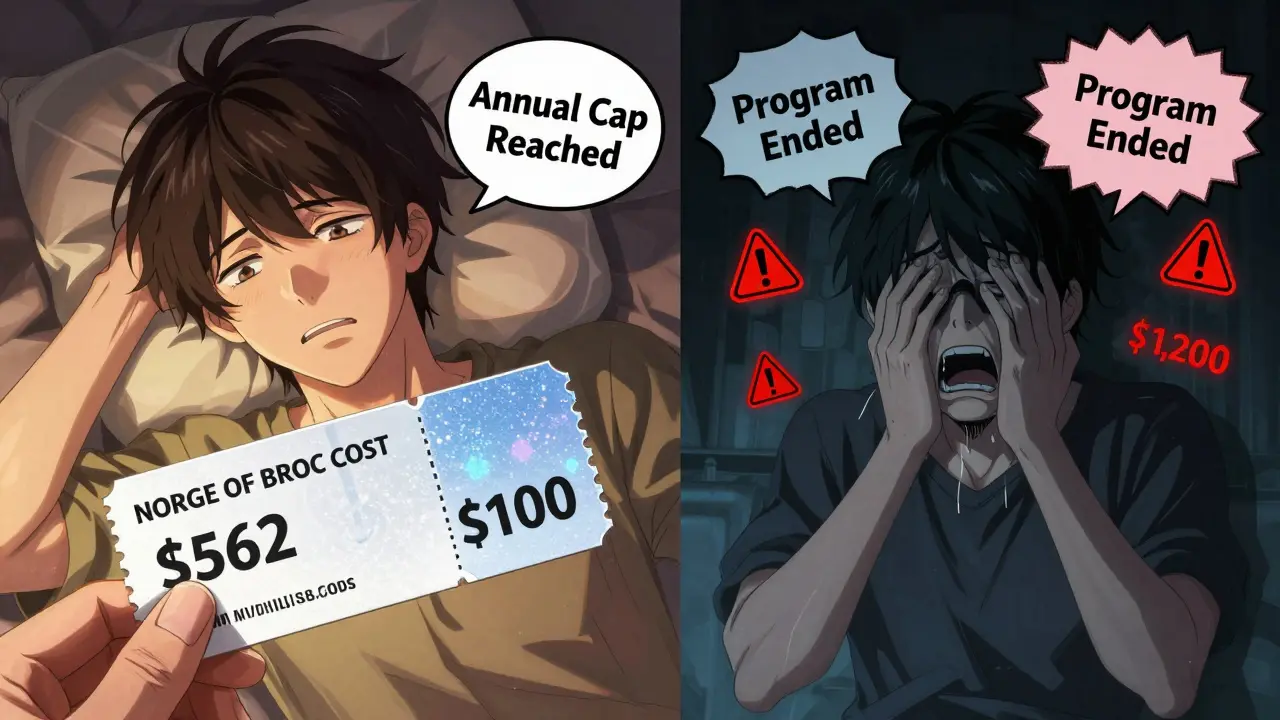

- Expiration dates: Most cards last 12 to 24 months. After that, you have to reapply. Some programs auto-renew. Others don’t. If you forget, your cost jumps back up overnight.

- Annual caps: The manufacturer might only cover up to $5,000 or $15,000 per year. If your drug costs $10,000 a year, you’ll pay the rest after hitting the cap.

- Accumulator programs: As mentioned, if your plan blocks the discount from counting toward your deductible, you might pay less monthly but still owe thousands by December.

- Program cancellation: Companies can stop a program anytime. One Reddit user shared that after Humira’s coupon ended, their monthly cost went from $100 to $1,200. No warning. No notice.

Always check the fine print. Look for terms like “annual limit,” “program end date,” and “insurance restrictions.”

Manufacturer Programs vs. Pharmacy Discount Cards

You’ve probably seen GoodRx or SingleCare ads. They offer discounts on both brand and generic drugs. So how do they compare?

| Feature | Manufacturer Savings Programs | Pharmacy Discount Cards (e.g., GoodRx) |

|---|---|---|

| Works with insurance? | Yes-only if you have private insurance | No-used instead of insurance |

| Discount depth | 70%-85% off | 30%-60% off |

| Drugs covered | Brand-name only | Brand and generic |

| Annual cap | Usually $5,000-$15,000 | None |

| Expiration | Yes-12-24 months | No |

| Eligibility restrictions | Excludes Medicare/Medicaid | Open to everyone |

Manufacturer programs give deeper discounts but come with more rules. Discount cards are simpler and available to anyone, but you won’t save as much. If you have private insurance and qualify, the manufacturer program is almost always better.

What Happens When the Program Ends?

It’s not if-it’s when. Companies change or end programs all the time. That’s why you need a backup plan.

- Ask your doctor about generic alternatives. Sometimes a generic version exists and works just as well.

- Check if your drug has a biosimilar. For example, Humira now has biosimilars that cost 40% less.

- Switch to a different drug in the same class. Your doctor might have options that are cheaper or have better savings programs.

- Use GoodRx or NeedyMeds to compare cash prices. Sometimes paying cash with a discount card is cheaper than waiting for a new manufacturer coupon.

Don’t wait until your card expires. Start planning three months ahead. Talk to your pharmacist. They see this happen every day.

Real Stories

A 58-year-old woman with rheumatoid arthritis used a manufacturer coupon for Enbrel. Her monthly cost dropped from $680 to $85. She used it for 18 months. Then the program ended. She had to switch to a biosimilar and now pays $150 per month-still less than before.

A man on Ozempic for diabetes saved $400 per month for two years. When his coupon expired, his insurance denied prior authorization. He called his doctor, switched to a different GLP-1 drug with a better coupon, and kept his savings.

But others weren’t so lucky. One Reddit user said after their copay card for a heart medication ended, they skipped doses for six months because they couldn’t afford it. That’s the dark side.

What’s Changing in 2026?

The rules are shifting. The Inflation Reduction Act capped insulin at $35 for Medicare users. That’s reducing reliance on coupons for insulin. Some states now require insurers to count manufacturer discounts toward deductibles. The federal government is considering similar rules.

But for now, if you have private insurance and a high-cost brand drug, these programs are still your best tool. Just don’t treat them like a permanent fix. Treat them like a temporary shield-use them wisely, plan ahead, and always have a backup.

Can I use a manufacturer savings program if I’m on Medicare?

No. Federal law prohibits pharmaceutical companies from offering copay assistance to people enrolled in Medicare, Medicaid, or other government health programs. This is to prevent incentives that could drive up costs for taxpayers. If you’re on Medicare, look into the Medicare Part D Low-Income Subsidy (Extra Help) program or use pharmacy discount cards like GoodRx instead.

Do I need a prescription to sign up for a manufacturer savings program?

Yes. You must have a current prescription for the specific brand-name drug you’re seeking help with. The program will ask for your prescriber’s name and the prescription details during enrollment. You can’t sign up in advance-only after your doctor has written the script.

What if my pharmacy says the coupon doesn’t work?

Some pharmacies don’t participate in certain programs, or their system might not recognize the card. Ask if they use a third-party administrator like ConnectiveRx. If not, try a different pharmacy-especially one that’s part of your insurer’s network. Many manufacturers list participating pharmacies on their website. Call ahead if you’re unsure.

Can I use a manufacturer coupon and a pharmacy discount card together?

No. You can only use one discount at a time. The pharmacy system will reject the second one. Choose the option that gives you the lowest price. Usually, the manufacturer coupon is better if you’re eligible. But if your coupon expired or was denied, use GoodRx to compare cash prices.

Are manufacturer savings programs safe and legal?

Yes, they’re legal for people with private insurance. They’re regulated and tracked by third-party administrators to ensure compliance with federal laws. However, they’re controversial because they help drug companies maintain high prices by reducing competition from generics. While they’re legal and useful for patients, experts warn they may contribute to long-term cost increases for insurance plans and employers.

Next Steps

If you’re currently paying high out-of-pocket costs for a brand drug:

- Check the manufacturer’s website for a savings program.

- Confirm your insurance is eligible (not Medicare/Medicaid).

- Enroll online and get your card.

- Use it at a participating pharmacy.

- Set a reminder for renewal-6 months before expiration.

- Ask your doctor or pharmacist: “Is there a cheaper alternative if this ends?”

These programs can save you thousands. But they’re not forever. Stay informed. Stay proactive. And never assume your discount will last.

Digital Raju Yadav

February 16, 2026 AT 17:18These manufacturer programs are just another way Big Pharma screws the public while pretending to help. In India, we see this same crap-drugs priced at 10x their production cost, then ‘discounts’ that vanish the moment you get dependent. It’s not charity, it’s a trap. You think you’re saving money? Nah. You’re locking yourself into a system where the company owns your health. And don’t even get me started on how they lobby to block generics. This isn’t healthcare. It’s a corporate feeding frenzy.

Carrie Schluckbier

February 16, 2026 AT 22:30Anyone else notice how every single one of these programs disappears right after you’ve been on the drug for 18 months? I swear, it’s like they have a calendar programmed into their servers. ‘Day 540: Trigger patient panic. Deploy insurance loophole. Profit.’ And don’t tell me it’s coincidence. The timing is too perfect. I think the pharma CEOs have a secret meeting once a year where they pick which drugs to kill the coupons on. It’s all calculated. They want you desperate.

Liam Earney

February 18, 2026 AT 04:40Look, I get it-these programs seem like a godsend when you’re staring down a $700 monthly bill for your rheumatoid arthritis meds, but let’s not pretend this is sustainable. The entire structure is built on a Ponzi scheme of third-party administrators, insurance loopholes, and regulatory blind spots. The manufacturer pays the discount, sure-but then they raise the list price by 15% the next year to compensate. You’re not saving money; you’re just delaying the inevitable financial collapse. And when the program ends? You’re left with a $1,200 bill and no safety net. It’s not a solution-it’s a temporary Band-Aid on a hemorrhage.

Geoff Forbes

February 18, 2026 AT 18:39As someone who actually read the fine print (unlike most of you), let me clarify: Accumulator adjustment programs are not ‘evil’-they’re actuarial necessities. If insurers had to count manufacturer discounts toward deductibles, premiums would skyrocket. The system is designed to incentivize cost-conscious behavior. You want to save? Use generics. Or better yet-don’t take brand-name drugs unless absolutely necessary. It’s not that complicated. Stop blaming pharma and start taking personal responsibility for your healthcare decisions.

Logan Hawker

February 19, 2026 AT 23:18Let’s be real: these programs are the reason pharmaceutical innovation is still alive. Without the revenue stream from these high-margin brand drugs-subsidized by patients who use copay cards-there’d be no R&D for the next generation of biologics. The system is flawed? Of course. But dismantling it won’t fix the root issue: drug pricing is broken because we’ve outsourced regulation to Wall Street. The real villain isn’t the manufacturer-it’s the insurance industry that refuses to count discounts toward out-of-pocket maxes. And yes, I’ve personally used these programs for my GLP-1. They saved my life. But I also know they’re a band-aid. The solution? Single-payer. Or at least, a federal cap on list prices. Until then, use the card. Just don’t romanticize it.

guy greenfeld

February 21, 2026 AT 19:16Think about it… what if the entire pharmaceutical model is a psychological experiment? You’re given a lifeline-$10 prescriptions, instant relief, hope-then, just as you become emotionally and physiologically dependent, it’s yanked away. You’re left gasping. And then? You’re told to ‘switch to generics’-but your body doesn’t respond the same. So you suffer. Or you go into debt. Or you stop taking it. And then… you get sick. Again. This isn’t capitalism. This is behavioral conditioning. They don’t just sell drugs. They sell dependency. And they profit from the collapse.

Adam Short

February 22, 2026 AT 22:03Man, I’ve seen this play out in the NHS and it’s the same damn story. Big Pharma comes in with their ‘helpful’ coupons, gets patients hooked, then leaves the government holding the bag when the program expires. It’s colonial economics wrapped in a white coat. And now they’re pushing this exact model in the US-because they know Americans won’t fight back until they’re bankrupt. Don’t be fooled. This isn’t generosity. It’s exploitation dressed up as empathy.

Steph Carr

February 23, 2026 AT 01:21Wow. So you’re telling me the system is designed to make you dependent on a coupon that expires? And then you’re supposed to ‘just switch’ to a cheaper drug? Like your body is a vending machine that can be reprogrammed? I’ve been on Ozempic for 2 years. I switched to a biosimilar last year. It cost me $1,500 out of pocket because my insurance didn’t count the coupon. I cried in the pharmacy parking lot. This isn’t healthcare. It’s a horror show. And we’re all just waiting for our turn to be the next victim.

Brenda K. Wolfgram Moore

February 24, 2026 AT 21:37If you’re using one of these programs, you’re already doing the right thing. Don’t let anyone make you feel guilty for it. You’re not gaming the system-you’re surviving it. I’ve helped dozens of people enroll in these programs. The real problem isn’t the coupons. It’s that we don’t have universal healthcare. Until we do, use every tool you can. Set reminders. Talk to your pharmacist. Save screenshots. And when the program ends? Start planning your next move immediately. You’re not weak for needing help. You’re smart for using it.

Agnes Miller

February 25, 2026 AT 23:24Just a quick tip: if your pharmacy says the coupon doesn’t work, ask them to manually enter the manufacturer’s BIN number. Most of the time it’s just a system glitch. Also, always check the expiration date on the card-some auto-renew, others don’t. I’ve had people show up with expired coupons and no backup plan. It’s heartbreaking. Talk to your pharmacist every refill. They know more than you think.