Insurance coverage: make your prescriptions more affordable

Your insurer might cover a drug — or they might make it a headache. I've seen people pay full price because they missed one detail. This page gives clear, practical moves you can use right now to lower costs and win coverage battles for men's health meds.

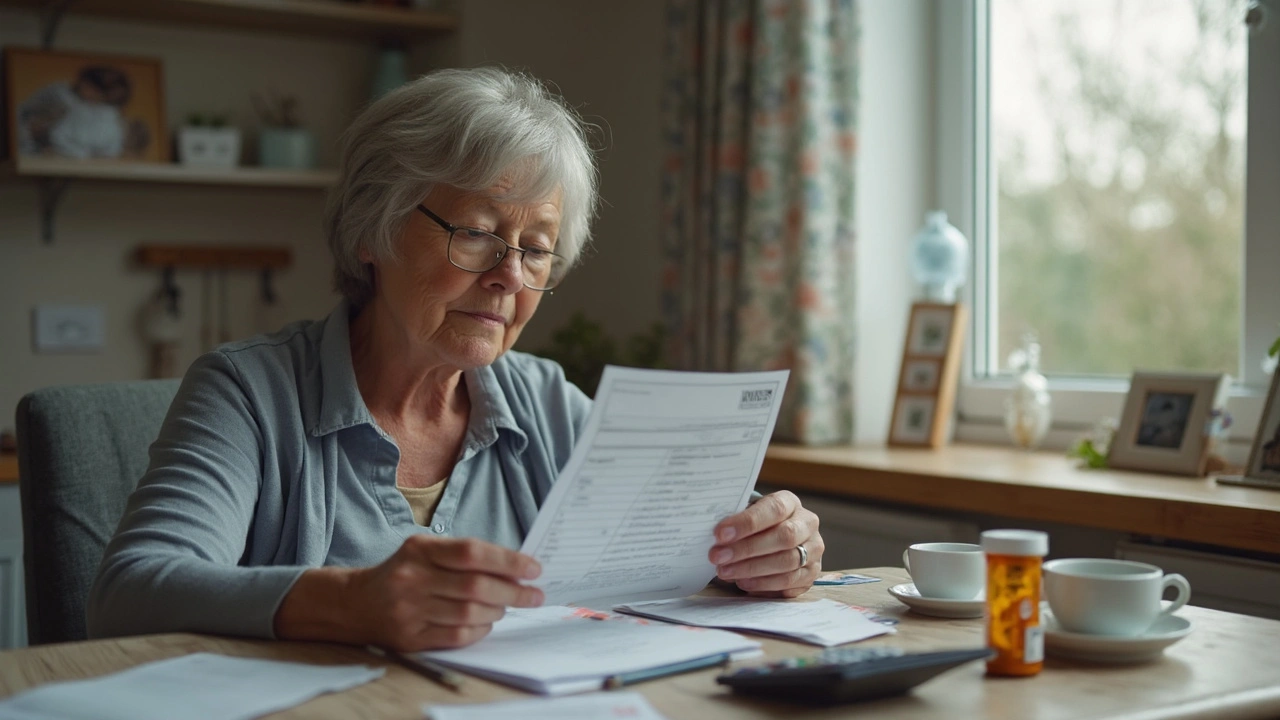

Start by checking the formulary. That’s the list of drugs your plan prefers. If your medication is on a lower tier or has a generic alternative, your copay drops a lot. Ask your pharmacist or log into your insurer’s member site and search the drug name. If a cheaper generic exists, talk to your doctor about switching — it often takes one sentence to change a prescription.

How to cut costs fast

Use mail-order or 90-day supplies for chronic meds. Many plans lower prices for a 3-month supply through their mail-order pharmacy. That saves time and often reduces copays. Also check manufacturer copay cards and patient assistance programs — drug makers sometimes cover most of your cost if you qualify. Don’t forget discount services like SingleCare or RxSaver when your insurance doesn’t help; they can beat out-of-pocket prices for a one-off fill.

Know when prior authorization or step therapy applies. Prior authorization means the insurer wants proof the drug is necessary. Step therapy forces you to try cheaper drugs first. If your doctor thinks the preferred path is unsafe or won’t work, ask them to submit a medical necessity letter. A clear letter citing past failures or side effects usually speeds approval.

When a claim is denied — what to do next

Denials are annoying but beatable. First, call the insurer and get the exact reason for denial and any required forms. Then ask your doctor to file an appeal with a focused medical justification. Keep records: dates, names, reference numbers. If the internal appeal fails, you can request an external review — an independent clinician reviews the case and often overturns denials that lack strong medical reason.

Watch for coding mistakes. Simple errors in diagnosis or drug codes cause denials. Your clinic or pharmacy can fix these quickly if you point them out. Also, ask the pharmacist if a Therapeutic Interchange is possible — they can suggest an equivalent drug your plan prefers without changing therapy.

Final quick checklist: 1) Check formulary and tiers, 2) Ask about generics, 3) Try mail-order for 90 days, 4) Use manufacturer aid or discount services, 5) If denied, get a medical necessity letter and appeal. These steps cover most common insurance headaches and save real money.

If you want, I can walk you through a sample appeal letter or help find patient assistance programs for a specific drug. Just tell me the medication and your insurer and I’ll point you in the right direction.

Azathioprine Cost, Insurance, and Financial Aid: What Patients Need to Know in 2025

Azathioprine is a vital medication for many fighting autoimmune disorders, but the price tag can be daunting. This guide uncovers the true cost of azathioprine therapy in 2025, explores why prices vary widely, dives deep into insurance hitches, and lays out clear financial aid options. You'll find practical tips to lower your out-of-pocket costs and actionable resources if you’re struggling with your prescription bills. Real numbers, honest breakdowns, and smart strategies for managing your medication spending.