Every time you pick up a generic prescription, you pay a copay. Maybe it’s $10. Maybe it’s $15. You think, ‘I’m paying for this, so it must be helping me meet my deductible.’ But here’s the truth: generic copays usually don’t count toward your deductible. They do count toward your out-of-pocket maximum. And that difference can cost you hundreds-or even thousands-of dollars if you don’t understand it.

What’s the difference between a deductible and an out-of-pocket maximum?

Your deductible is the amount you pay before your insurance starts sharing the cost of covered services. For example, if your deductible is $3,000, you pay the first $3,000 of medical and prescription costs yourself. After that, your plan kicks in with coinsurance.

Your out-of-pocket maximum is the most you’ll ever pay in a year for covered services. Once you hit that number, your insurance pays 100% of everything else for the rest of the year. For 2025, the federal limit is $9,200 for an individual and $18,400 for a family.

Here’s the key: all your cost-sharing-deductibles, coinsurance, and copays-counts toward your out-of-pocket maximum. But only your deductible payments count toward your deductible. That means if you pay $10 copays for 200 prescriptions in a year, you’ve paid $2,000-but that $2,000 doesn’t shrink your $3,000 deductible. It only helps you inch closer to your $9,200 out-of-pocket maximum.

Why does this confusion exist?

Before 2014, copays didn’t count toward anything. You paid them, and they vanished-no progress on your deductible, no progress on your out-of-pocket max. People with chronic conditions like diabetes or high blood pressure were stuck paying the same copay every month, year after year, without ever getting relief.

The Affordable Care Act fixed that. Starting in 2014, all new plans had to include an out-of-pocket maximum, and all in-network cost-sharing had to count toward it. That was a huge win. But it didn’t change how deductibles work. So now you have a system where:

- You pay $10 for a generic pill → it counts toward your out-of-pocket max

- But it doesn’t reduce your $3,000 deductible

- So you could pay $5,000 in copays and still owe $3,000 more before coinsurance starts

This creates what experts call a “valley of confusion.” A 2023 survey by America’s Health Insurance Plans found that 68% of people think their prescription copays count toward their deductible. Only 22% got it right.

How your plan type changes everything

Not all health plans are built the same. There are three main models:

- Single deductible (27% of employer plans): One amount covers both medical and prescriptions. If you pay $100 for a doctor visit and $15 for a prescription, both go toward the same deductible. In these plans, you usually don’t have copays-you pay full price until you hit the deductible, then coinsurance kicks in.

- Separate deductibles (37% of plans): You have one deductible for doctor visits and hospital care, and another for prescriptions. You might have a $1,500 medical deductible and a $750 prescription deductible. Your $10 generic copay counts toward your prescription deductible, not your medical one. Once you hit the prescription deductible, you start paying copays that count toward your overall out-of-pocket maximum.

- Copay-only (no prescription deductible) (36% of plans): You pay your $10 copay right away, no matter what. But again, that $10 doesn’t reduce your medical deductible. It only counts toward your out-of-pocket maximum.

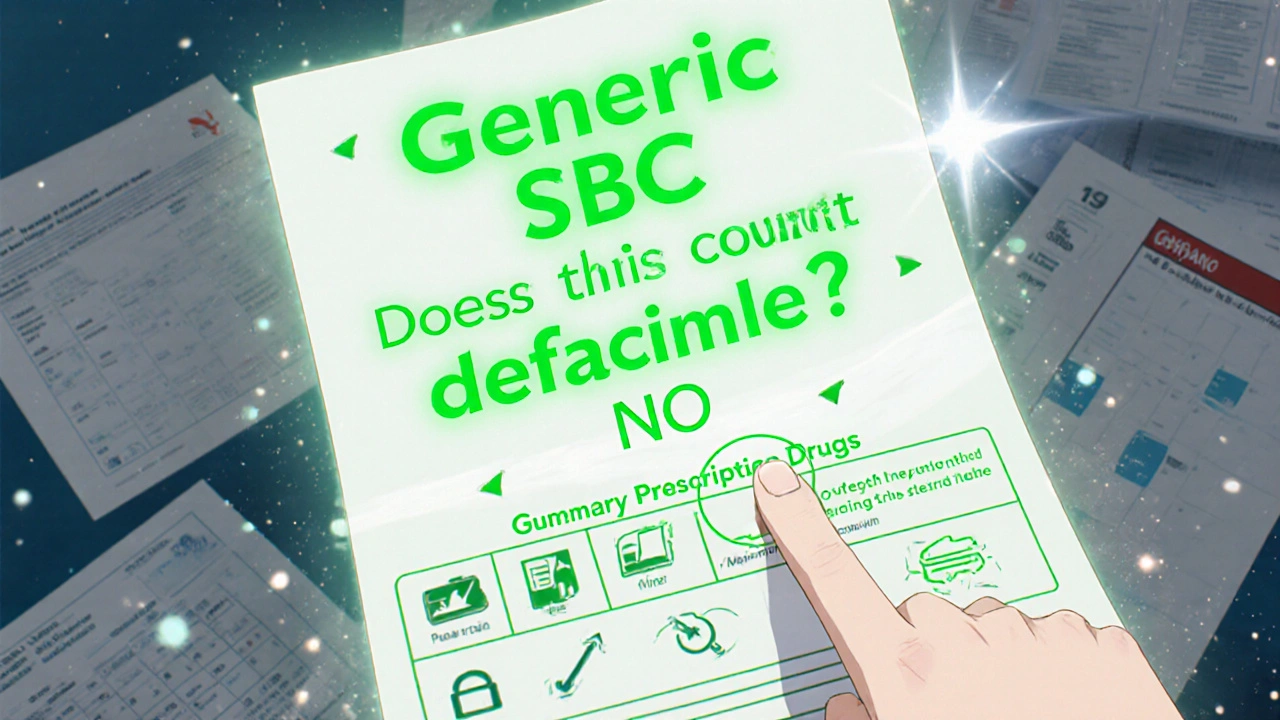

Most people don’t realize their plan type until they’re already paying out of pocket. That’s why reviewing your Summary of Benefits and Coverage (SBC) during open enrollment isn’t optional-it’s critical.

What to look for in your plan documents

Your plan’s SBC is required by law to use a standardized format. Look for these exact phrases:

- “Does this payment count toward my deductible?” - Check the row for “Generic Prescription Drugs.”

- “What is my out-of-pocket maximum?” - Confirm it includes copays.

- “Are there separate deductibles for medical and prescription drugs?” - If yes, you’re in the 37% group.

Also check your Explanation of Coverage document. It’s longer, but it spells out exactly how each payment works. Don’t skip this. One user on HealthCare.gov said she paid $2,500 in copays over a year-thinking she’d met her $2,000 deductible-only to find out she still owed $2,000 when she needed an MRI.

Real-world impact: When this matters most

Imagine you have type 2 diabetes. You take metformin, insulin, and a blood pressure pill-all generics. That’s three copays a month. At $15 each, that’s $45 a month, or $540 a year. If your plan has a separate prescription deductible of $750, you’re paying full price until you hit that. But if your plan has no prescription deductible, you’re paying $540 in copays that count toward your out-of-pocket maximum.

In the first case, you’re not getting closer to your medical deductible. In the second, you’re building toward your $9,200 limit. Once you hit it, your insulin becomes free for the rest of the year.

That’s why people with chronic conditions love the post-ACA rules. One Reddit user wrote: “Before 2014, my $15 insulin copays didn’t get me closer to anything. Now I reached my $8,500 out-of-pocket max last year-and my meds were free after June.”

What’s changing in 2025 and beyond

The government is pushing for clearer communication. Starting in 2025, insurers must highlight in plain language whether prescription copays count toward your deductible. The Department of Health and Human Services also launched pilot programs in five states testing “integrated deductibles”-where prescription costs, including copays, count toward one single deductible.

Early results show 28% higher medication adherence. That means people actually fill their prescriptions because they know they’re making progress.

Industry analysts predict that by 2027, 60% of major insurers will offer at least one plan where generic copays count toward the deductible. Why? Because consumers are tired of the confusion. But there’s a catch: simplifying this could raise premiums by 3-5%, according to the American Hospital Association.

So the trade-off isn’t just about clarity-it’s about cost. Simpler rules might mean higher monthly payments.

What you should do right now

Don’t wait for open enrollment. Check your plan details today:

- Log into your insurer’s website and find your SBC.

- Look for the “Generic Prescription Drugs” row.

- Check the column labeled “Does this payment count toward my deductible?”

- If it says “No,” then your copays only count toward your out-of-pocket maximum.

- If it says “Yes,” then you’re in the minority-your plan is simpler than most.

If you’re on a high-deductible plan and take regular medications, track your copay spending. Add it up monthly. If you’re close to your out-of-pocket maximum, you might be just a few prescriptions away from free care for the rest of the year.

And if you’re still confused? Call your insurer. Ask: “Do my generic prescription copays count toward my deductible? Or only my out-of-pocket maximum?” Write down their answer. You’re not being annoying-you’re protecting your wallet.

Bottom line

Generic copays are not a waste. Even if they don’t shrink your deductible, they’re still working for you-by pushing you closer to your out-of-pocket maximum. Once you hit that ceiling, your medications become free. That’s the real win.

Stop assuming your copays count toward your deductible. Check your plan. Track your spending. And don’t let confusion cost you more than you have to.

Rodney Keats

November 16, 2025 AT 03:06So let me get this straight-I pay $15 every month for my diabetes meds, and the insurance company’s like, ‘lol nice try, that doesn’t count toward your $3k deductible’? Thanks, capitalism. At this point, my copays are just rent I pay to the hospital-industrial complex. At least my insulin’s free after June. I guess I’m winning? 🤡

Laura-Jade Vaughan

November 18, 2025 AT 00:26OMG this is SO important 😭 I literally just found out my copays DON’T count toward my deductible-after paying $2k+ this year 🥲 I’ve been crying into my metformin bottle for months. Thank you for the SBC tip!! I’m printing it out and laminating it. 💅💊 #HealthLiteracy #NoMoreConfusion

Jennifer Stephenson

November 19, 2025 AT 01:28Check your plan. Know your terms. Do it now.

Segun Kareem

November 20, 2025 AT 14:02This is the kind of systemic invisibility that breaks people. In Nigeria, we don’t have deductibles-we have ‘can you afford this?’ But here, the system is designed to confuse you into silence. Your copay isn’t wasted-it’s a brick in the wall that eventually lets you walk free. Keep building. You’re closer than you think.

Philip Rindom

November 20, 2025 AT 16:10Honestly, I thought my $10 copays were eating into my deductible too. Had no idea they were just… sitting there like unpaid parking tickets. Thanks for the clarity. Also, I just called my insurer and they said ‘yes’ to deductible inclusion-turns out I’m in the 27% club. Who knew? 😅

Jess Redfearn

November 20, 2025 AT 21:14Wait so if I pay $10 for a pill, and it doesn’t count toward my deductible, does that mean the insurance company just keeps it? Like… for fun? Are they hoarding my $10s? I need to know where my money is going.

Ashley B

November 21, 2025 AT 22:48This is all a scam. The government and Big Pharma designed this to make you think you’re getting somewhere while they drain your bank account. They know you’re too tired to read the SBC. They count on it. They’re laughing. I’ve seen the documents. This isn’t healthcare-it’s a financial trap with a stethoscope.

Sharon Campbell

November 22, 2025 AT 02:03lol i thought my copays were helping me get to my deducible. i just paid 3k in pills and still owe 2k. oops. maybe next year i’ll read the tiny print. 🤦♀️

sara styles

November 22, 2025 AT 15:57You think this is bad? Wait until you find out that some insurers are secretly reclassifying generic drugs as ‘non-preferred’ after you’ve been paying the copay for years. Then they jack up the price and say ‘oh, you didn’t check the formulary update from April 2023?’ That’s not a glitch-that’s predatory design. I’ve filed 3 complaints with the state AG. They’re all ignored. This is how people die quietly. Don’t let them do this to you.

Brendan Peterson

November 23, 2025 AT 04:39There’s a nuance here that’s often missed: even in plans with separate deductibles, the out-of-pocket maximum still absorbs ALL cost-sharing. So while your copay doesn’t reduce your prescription deductible, it does reduce your total liability. The real issue is transparency, not structure. The ACA got the structure right; the problem is the execution and communication. You need to know your plan type. Period.

Jessica M

November 24, 2025 AT 05:50Thank you for this clear, evidence-based explanation. As a healthcare administrator, I see patients make life-altering financial decisions based on this exact misunderstanding. The 2025 plain-language requirements are a necessary step. Please share this with anyone on a high-deductible plan. This information prevents medical bankruptcy. Your SBC is not a document-it is a shield. Use it.